Thank you a ton for taking the time to patiently explain all this. So here's where I'm currently stuck. Or actually, I'm stuck in a few places right now:

(1) This is less relevant to this particular debate, but it's highly relevant to the actual opt-out page. On the webpage, I don't see the word "sign" at all. I imagine merely filling in your name into that box and clicking "Submit" doesn't turn your name into your signature. In fact the page explicitly says "the information for the Chase account holder"... which need not be you, so it definitely can't account as the account holder's signature... right? So regardless of the electronic vs. paper issue we still seem to have a pretty fundamental problem that even this page hasn't been signed by the account owner in any shape or form.

(2) This is more specific to our discussion. So if there were a signature box on that form and you put your name in as your electronic signature, what exactly would you have electronically signed? I never (I think) said that you wouldn't have electronically signed anything at all, but rather, that what you signed electronically would not have been the agreement of interest, i.e. the one to be sent to Chase. Rather, as I see it, you would have signed something separate from that -- more like a contract (if it even counts as a contract... not sure how considerations play into this, given it's free) with whoever's running that website, to write your intended letter, put a copy of your signature on it, and basically impersonate you in sending this to Chase. Leaving aside the question of whether this is fraud (which is also something I've been pondering, since Chase would seem to think it came from you), that would mean you never signed that agreement at all. At best, I feel you could only try to argue you gave this site a power of attorney to represent you... not sure how valid a court would find that with the form currently as-is. So I'm still struggling to see how you could claim to have signed the agreement sent to Chase.

(3) The "electronic agent" thing seems like a red herring (I'm not sure why you brought it up) since it seems to refer the software, not the human on the other side.

(4) Is this really a question of whether the agreement is valid "solely because it is in electronic form"? In my view it's a question of whether it's valid "because its terms for it taking effect are followed". One of the terms was signing it in electronic form, but that's just (if you will) an implementation detail the way I see it. This may be my CS-y brain but the law sounds like it's intended to address governmental "discrimination" against electronic signatures (if you will), not private decisions on how to form valid agreements. It seems kind of like how, even though the law requires that a $100 bill be valid as legal tender for all private debts, no store owner is obligated to accept a $100 bill as a payment of $100 for goods you haven't officially bought yet.

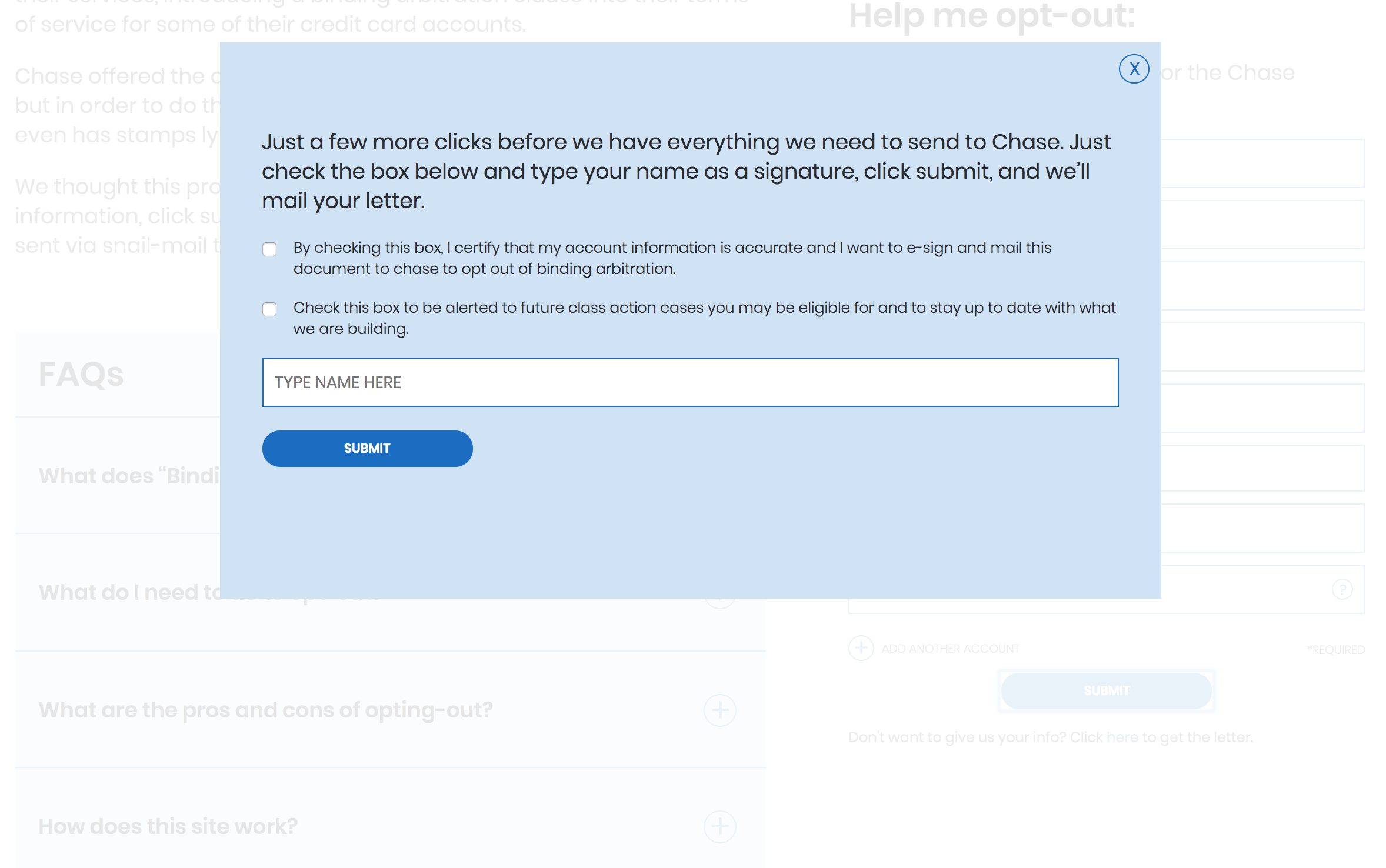

You assumed that the process is done when you click that first Submit button, but it is not. There is an e-signing step that makes it clear what you are doing and what you are signing. [0]

I also did not realize this and it probably would have prevented me from posing the question in the first place. Seems like it would be clearer for the first button say "Click to sign" or something (other than "Submit").

{kind=link}

(1) This is less relevant to this particular debate, but it's highly relevant to the actual opt-out page. On the webpage, I don't see the word "sign" at all. I imagine merely filling in your name into that box and clicking "Submit" doesn't turn your name into your signature. In fact the page explicitly says "the information for the Chase account holder"... which need not be you, so it definitely can't account as the account holder's signature... right? So regardless of the electronic vs. paper issue we still seem to have a pretty fundamental problem that even this page hasn't been signed by the account owner in any shape or form.

(2) This is more specific to our discussion. So if there were a signature box on that form and you put your name in as your electronic signature, what exactly would you have electronically signed? I never (I think) said that you wouldn't have electronically signed anything at all, but rather, that what you signed electronically would not have been the agreement of interest, i.e. the one to be sent to Chase. Rather, as I see it, you would have signed something separate from that -- more like a contract (if it even counts as a contract... not sure how considerations play into this, given it's free) with whoever's running that website, to write your intended letter, put a copy of your signature on it, and basically impersonate you in sending this to Chase. Leaving aside the question of whether this is fraud (which is also something I've been pondering, since Chase would seem to think it came from you), that would mean you never signed that agreement at all. At best, I feel you could only try to argue you gave this site a power of attorney to represent you... not sure how valid a court would find that with the form currently as-is. So I'm still struggling to see how you could claim to have signed the agreement sent to Chase.

(3) The "electronic agent" thing seems like a red herring (I'm not sure why you brought it up) since it seems to refer the software, not the human on the other side.

(4) Is this really a question of whether the agreement is valid "solely because it is in electronic form"? In my view it's a question of whether it's valid "because its terms for it taking effect are followed". One of the terms was signing it in electronic form, but that's just (if you will) an implementation detail the way I see it. This may be my CS-y brain but the law sounds like it's intended to address governmental "discrimination" against electronic signatures (if you will), not private decisions on how to form valid agreements. It seems kind of like how, even though the law requires that a $100 bill be valid as legal tender for all private debts, no store owner is obligated to accept a $100 bill as a payment of $100 for goods you haven't officially bought yet.